This article is for educational and informational purposes only and is not investment advice. The views expressed are those of the author and do not constitute recommendations to buy, sell, or hold any securities or digital assets. Please consult with a qualified financial advisor before making investment decisions.

The Regulatory Clarity We’ve Been Waiting For

For years, the stablecoin market has operated in a regulatory twilight zone—a $300 billion ecosystem built on legal ambiguity. Issuers navigated a maze of conflicting guidance from the SEC, CFTC, and state regulators, while institutional investors watched from the sidelines, unwilling to commit capital without clear rules of the road.

That era ended on July 18, 2025, when the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act became law. This landmark legislation doesn’t just regulate stablecoins—it legitimizes them as a fundamental component of the U.S. financial system. And the implications are nothing short of transformative.

As someone who has spent years at the intersection of traditional finance and digital assets, I’ve watched this regulatory evolution with keen interest. The GENIUS Act represents more than just legal clarity; it’s a strategic bet on the future of money itself. Let me explain why this matters—and what it means for investors, institutions, and the broader financial landscape.

What the GENIUS Act Actually Does

At its core, the GENIUS Act creates a comprehensive federal framework for “payment stablecoins”—digital assets designed to maintain a stable value relative to the U.S. dollar. But the devil, as always, is in the details.

The Act makes a critical definitional move: it explicitly states that compliant stablecoins are neither securities nor commodities. This legislative carve-out removes them from SEC and CFTC jurisdiction, placing oversight squarely with banking regulators. For an industry that has spent years fighting jurisdictional battles, this clarity is revolutionary.

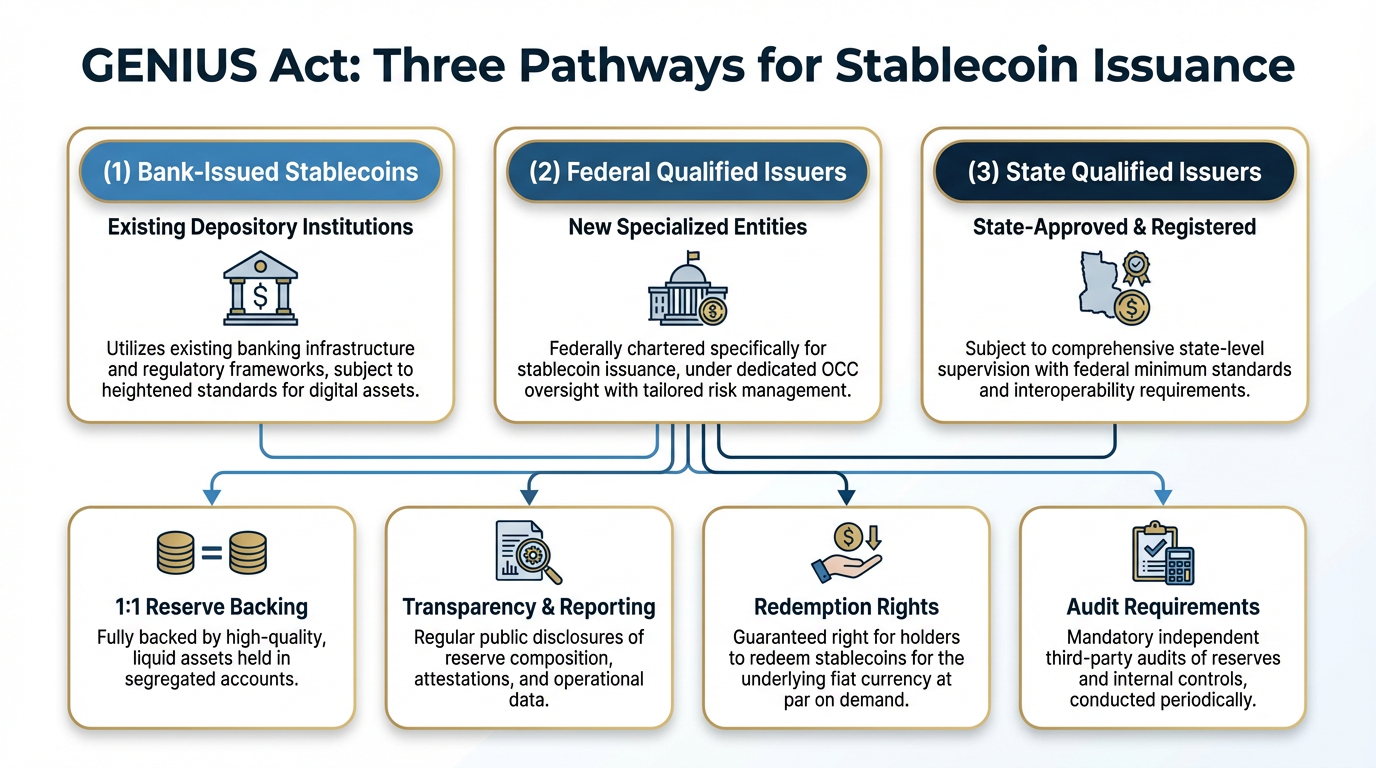

The framework establishes three pathways for issuing stablecoins:

- Bank-issued stablecoins through approved subsidiaries of insured depository institutions

- Federal qualified issuers—non-bank entities that receive special OCC charters

- State qualified issuers operating under certified state frameworks (with federal oversight triggered at $10 billion in circulation)

This dual federal-state structure is elegant. It allows innovation at the state level while ensuring systemic oversight for large players. It’s federalism applied to digital finance.

But the real teeth of the Act lie in its operational requirements. Issuers must maintain 1:1 reserves in high-quality liquid assets—U.S. dollars, Treasury bills, and similar instruments. These reserves must be segregated, audited monthly, and published transparently. Rehypothecation is prohibited. Redemption rights are guaranteed. And in bankruptcy, stablecoin holders get priority claims on reserves.

Perhaps most importantly, the Act prohibits issuers from paying interest on stablecoin holdings. This provision, while controversial, prevents stablecoins from directly competing with FDIC-insured bank deposits—a compromise that secured banking industry support for the legislation.

The Institutional Floodgates Are Opening

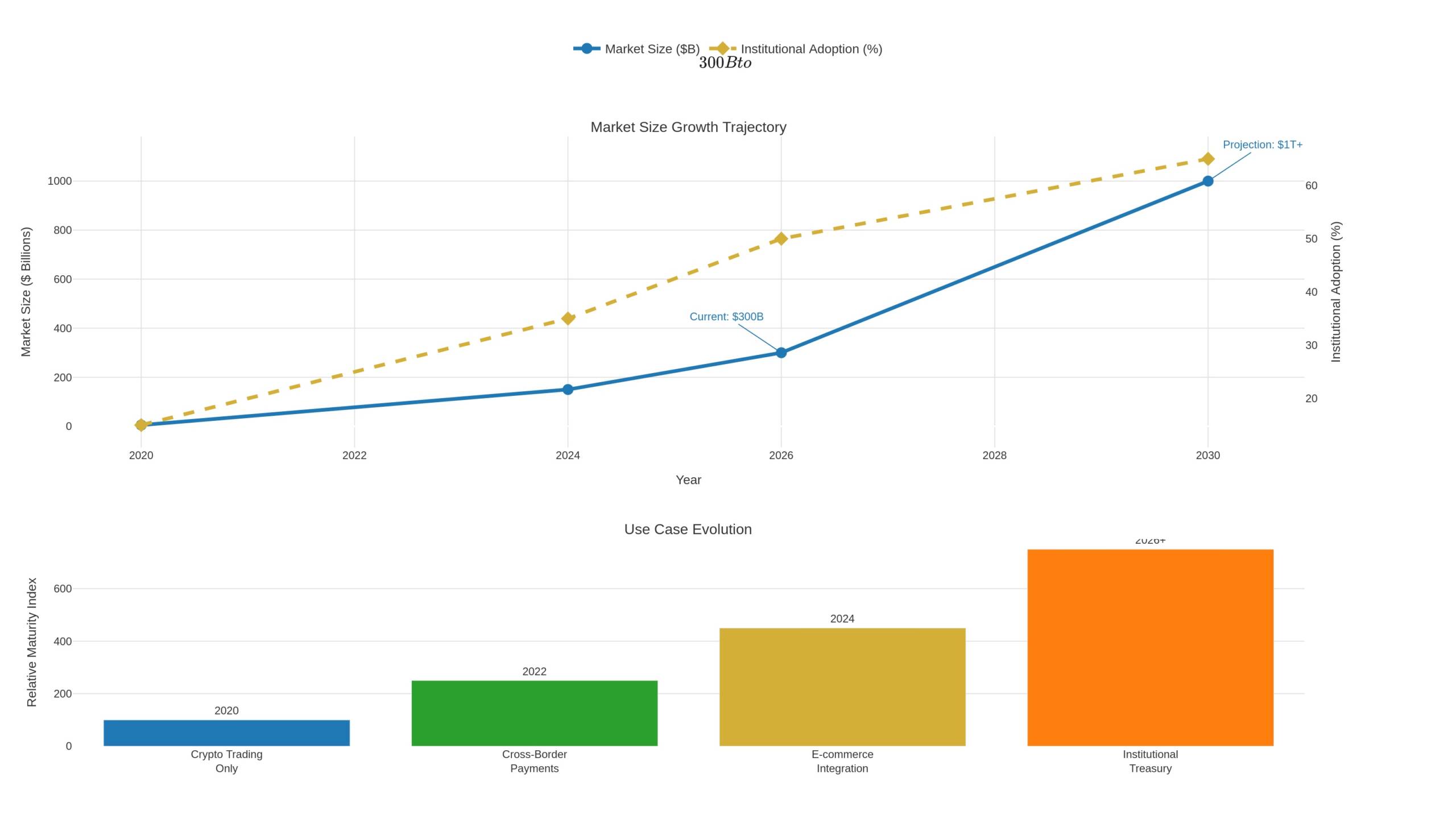

The market response has been swift and decisive. By early 2026, the stablecoin market had already surpassed $300 billion in market capitalization, with projections suggesting it could exceed $1 trillion by year-end. That’s not hype—it’s the natural consequence of removing regulatory uncertainty.

Consider the institutional adoption trajectory. A recent survey found that while only 13% of financial institutions were using stablecoins in 2025, 54% of non-users planned to adopt them within 12 months. That’s not a gradual shift—it’s a stampede.

We’re already seeing the evidence. Visa’s stablecoin-linked card spending hit a $3.5 billion annualized run rate in late 2025—a 460% year-over-year increase. BlackRock, Mastercard, and major banks are integrating stablecoins into settlement infrastructure. B2B stablecoin payment volumes surged from under $100 million monthly in early 2023 to over $6 billion by mid-2025.

This isn’t just about crypto trading anymore. The real revolution is happening in real-world payments—cross-border remittances, B2B settlements, treasury management, and financial inclusion. Stablecoins offer near-instant, 24/7 settlement at a fraction of traditional costs. Remittance fees drop from 6.5% to under 1%. Settlement times collapse from days to seconds.

At Savanti Investments, we’ve been tracking this evolution closely through our QuantAI™ platform, which analyzes market microstructure and liquidity patterns across both traditional and digital asset markets. The data is unambiguous: stablecoins are becoming critical infrastructure for global capital flows.

The Competitive Landscape Is Shifting

The GENIUS Act doesn’t just regulate the existing market—it reshapes the competitive dynamics entirely.

Today, Tether (USDT) and Circle’s USD Coin (USDC) dominate, with market caps of approximately $186.7 billion and $75.1 billion respectively. But USDC has been growing faster, largely because Circle has positioned itself as the compliant, transparent alternative. The GENIUS Act validates that strategy.

More importantly, the Act opens the door for traditional banks to enter the market at scale. Banks have regulatory infrastructure, customer trust, and massive balance sheets. They can issue stablecoins through approved subsidiaries, leveraging existing compliance frameworks and distribution channels.

This creates fascinating competitive tension. Will incumbent fintech issuers maintain their first-mover advantage? Or will banks use their regulatory familiarity and customer relationships to capture market share? My bet: we’ll see both—a bifurcated market where fintech issuers dominate crypto-native use cases while banks capture mainstream payment flows.

The prohibition on interest payments adds another wrinkle. While issuers can’t pay direct yield, they can offer other incentives—rewards programs, fee rebates, integrated financial services. This creates room for product innovation and differentiation beyond simple yield competition.

Global Implications and the Dollar’s Digital Future

The GENIUS Act isn’t just domestic policy—it’s a strategic move in the global competition for digital currency dominance.

The European Union’s Markets in Crypto-Assets (MiCA) regulation, which took effect around the same time, shares many principles with the GENIUS Act: 1:1 reserves, redemption rights, transparency requirements. This regulatory convergence is creating a transatlantic framework for stablecoin adoption, with the U.S. dollar and euro as the primary reference currencies.

But here’s the strategic insight: by providing regulatory clarity for dollar-denominated stablecoins, the U.S. is extending the dollar’s reach into the digital economy. Every USDC or compliant USDT transaction reinforces dollar dominance in global commerce. In high-inflation economies, dollar stablecoins provide wealth preservation and access to the global financial system—digital dollarization at scale.

This matters enormously in the context of Central Bank Digital Currencies (CBDCs). While China has deployed the digital yuan and other nations experiment with CBDCs, the U.S. has taken a different path: enabling private-sector innovation within a regulated framework. The GENIUS Act effectively makes compliant stablecoins a market-driven alternative to CBDCs—preserving privacy, fostering competition, and maintaining the dollar’s global role without direct government issuance.

It’s a brilliant strategic play, and one that aligns with American principles of market-based innovation.

The Risks We Can’t Ignore

Of course, no regulatory framework is perfect, and the GENIUS Act has legitimate critics.

Consumer advocates worry that the prohibition on interest payments creates an unlevel playing field. While banks offer FDIC insurance on deposits, stablecoin holders get no such protection—yet they also can’t earn yield. This could disadvantage consumers, particularly in a high-interest-rate environment.

Traditional banks fear deposit flight. If customers can hold stablecoins on user-friendly platforms with integrated financial services, why keep money in low-yield savings accounts? The banking industry has lobbied aggressively to ensure the interest prohibition is enforced strictly, but the competitive threat remains.

There are also implementation challenges. The Act requires state regulatory regimes to be certified as “substantially similar” to federal standards—a process that could take years and create fragmentation. The $10 billion threshold for federal oversight might be too high, allowing systemically important issuers to operate under less rigorous state supervision.

And then there’s the question of innovation. By imposing strict reserve requirements and prohibiting rehypothecation, the Act limits issuers’ ability to generate revenue. This could constrain business models and slow innovation, particularly for smaller players.

These are real concerns, and they’ll need to be addressed through regulatory refinement and market evolution. But they don’t negate the fundamental achievement: the U.S. now has a workable framework for integrating stablecoins into the financial system.

What This Means for Investors and Institutions

So what should investors and institutions do with this information?

First, recognize that stablecoins are now infrastructure, not speculation. The GENIUS Act transforms them from a regulatory gray area into a regulated financial product. This changes the risk profile fundamentally. Institutional allocators who have been sitting on the sidelines now have a clear path to participation.

Second, watch the competitive dynamics. The next 12-24 months will determine which issuers—fintech or traditional banks—capture market share. Circle’s compliance-first strategy looks prescient. Tether’s dominance may erode if it can’t demonstrate full compliance. And we’ll likely see major banks launch their own stablecoins, creating new competitive pressures.

Third, think about use cases beyond crypto trading. The real value creation will happen in payments, remittances, B2B settlements, and treasury management. Companies that integrate stablecoins into their payment infrastructure will gain efficiency advantages. Investors should look for businesses positioned to capitalize on this shift.

Fourth, consider the geopolitical dimension. Dollar-denominated stablecoins extend U.S. financial influence globally. This has implications for everything from sanctions enforcement to monetary policy transmission. Investors with international exposure should understand how stablecoin adoption affects currency dynamics and capital flows.

At Savanti Investments, we’re integrating stablecoin market data into our QuantAI™ models, tracking liquidity patterns, adoption metrics, and cross-market correlations. Our SavantTrade™ platform is exploring stablecoin-based settlement for certain strategies, reducing friction and improving capital efficiency. And through Convirtio, we’re helping clients understand how stablecoins fit into broader digital transformation strategies.

This isn’t just about crypto anymore. It’s about the future of money, payments, and global finance.

The Road Ahead

The GENIUS Act is a beginning, not an ending. Implementation will take time. Regulatory guidance will evolve. Market structures will adapt. But the direction is clear: stablecoins are becoming a permanent, regulated component of the U.S. financial system.

This is a rare moment when regulatory clarity creates genuine opportunity. The institutions that move decisively—understanding the framework, building compliant infrastructure, and integrating stablecoins into their operations—will gain significant competitive advantages.

The question isn’t whether stablecoins will become mainstream. The GENIUS Act has answered that. The question is: who will capture the value as this $300 billion market grows to $1 trillion and beyond?

The race is on. And the winners will be those who recognize that we’re not just witnessing regulatory change—we’re witnessing the digitization of the dollar itself.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice. The content is not intended to be a substitute for professional financial advice. The author and Savanti Investments do not recommend that any particular digital asset, security, or investment strategy is suitable for any specific person. Investing in digital assets, including stablecoins, involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Before making any investment decision, you should conduct your own research and consult with a qualified financial advisor.

Regulation D, Rule 506(c) Notice: Certain investment opportunities mentioned in this article may be offered pursuant to an exemption from registration under Regulation D, Rule 506(c) of the Securities Act of 1933. Such offerings are limited to accredited investors only. This article does not constitute an offer to sell or a solicitation of an offer to buy any securities. Any such offer or solicitation will be made only by means of a confidential private placement memorandum and related documents.