Disclaimer: This article is for educational and informational purposes only and is not investment advice. The views expressed are those of the author and do not constitute recommendations to buy or sell any securities or assets. Please consult with a qualified financial advisor before making investment decisions.

The markets don’t like uncertainty. And right now, uncertainty is all we have.

Over the past three weeks, Brent crude has surged more than 28%, the VIX has climbed nearly 20%, and gold has quietly added another 4% to its already impressive run. These aren’t just numbers on a screen—they’re the market’s way of screaming that something fundamental has shifted. The long-simmering tensions between the United States and Iran have erupted from shadow conflict into overt interstate warfare, and the financial implications are only beginning to unfold.

This isn’t your typical geopolitical headline that fades in a news cycle. When one-fifth of the world’s oil supply flows through a 21-mile-wide chokepoint that Iran has explicitly threatened to close, when Saudi oil fields are dodging ballistic missiles, and when the US Navy is planning convoy escorts through the Strait of Hormuz, we’re not talking about tail risk anymore. We’re talking about a material repricing of global risk across every asset class.

The question isn’t whether this conflict will impact your portfolio. It already has. The question is: what do you do about it?

What’s Happening: From Shadow War to Open Conflict

The escalation has been swift and severe. What began as a “shadow conflict” characterized by proxy warfare and covert operations has transformed into direct military engagement. US-Israeli strikes on Iranian territory have been met with retaliatory attacks across the region—from drone strikes on Saudi Arabia’s Shaybah oil field to attacks on commercial vessels in the Persian Gulf.

The market data tells the story with brutal clarity. Between February 19 and March 11, WTI crude jumped 31%, while the S&P 500 shed 1.25% amid wild daily swings. The VIX, Wall Street’s fear gauge, spiked from 20 to 24—a 20% increase that signals investors are scrambling for protection.

But here’s what makes this different from past Middle East flare-ups: the direct threat to energy infrastructure. Multiple commercial vessels have been struck. Airlines are rerouting flights thousands of miles to avoid Iranian airspace, burning extra fuel and adding hours to flight times. The region’s travel and tourism sector is hemorrhaging an estimated $600 million per day. And the International Energy Agency has already authorized the release of 400 million barrels from strategic reserves—a record deployment that underscores just how serious this has become.

When the IEA pulls that trigger, it’s not a drill. It’s an acknowledgment that we’re staring down the barrel of what could be “the largest supply disruption in the history of oil markets.”

Why It Matters: The Strait of Hormuz Is the World’s Jugular

Geography is destiny, and in this case, geography is a 21-mile-wide strait that carries 20% of global oil and LNG trade. The Strait of Hormuz isn’t just a shipping lane—it’s the circulatory system of the global economy. And right now, that system is under direct threat.

Iran’s threat that “no oil will pass through the strait” isn’t bluster. It’s a strategic weapon. A prolonged blockade would put 15-20% of global oil supply at risk, dwarfing the disruption from the Russia-Ukraine war and potentially triggering a global recession.

The ripple effects are already visible. Saudi Arabia is rerouting maritime trade to Red Sea ports. Insurance premiums for vessels transiting the Gulf have skyrocketed. And energy companies are dusting off contingency plans that haven’t been needed since the Gulf War.

But the energy shock is just the first-order effect. The second-order effects—inflation, monetary policy paralysis, supply chain chaos—are where things get truly complicated.

The Central Bank Dilemma: Stagflation’s Ugly Return

Here’s the nightmare scenario keeping central bankers up at night: sustained high oil prices could add 0.6 to 0.7 percentage points to global inflation, just as they were finally making progress on bringing prices down. It’s a supply-side shock that acts like a tax on consumers and businesses, dampening demand while simultaneously pushing up prices.

The textbook response would be to tighten monetary policy to anchor inflation expectations. But tightening into a supply shock risks turning a slowdown into a recession. It’s the classic stagflation trap—stagnant growth plus high inflation—and there’s no good playbook for it.

The Federal Reserve is caught in the crossfire. President Trump is publicly pressuring the Fed to cut rates to offset the energy price spike. But cutting rates while inflation is accelerating would undermine the Fed’s credibility and risk unanchoring inflation expectations. It’s a lose-lose scenario, and the market knows it.

This is why the VIX is elevated. It’s not just about oil prices. It’s about the realization that the policy tools we’ve relied on for decades might not work in this environment.

Investment Implications: Navigating the Minefield

So what’s an investor to do? Panic selling is rarely the answer—historical data shows that equity markets typically recover from geopolitical shocks within weeks or months. But this isn’t a typical shock, and a disciplined reassessment of portfolio positioning is warranted.

The Winners

Defense and Aerospace: This is the most obvious beneficiary. Global defense spending is surging, with the US, Germany, and Japan all approving record or near-record budgets. Companies involved in munitions, missile defense, and advanced military systems are seeing multi-year order backlogs. This isn’t a trade—it’s a structural shift.

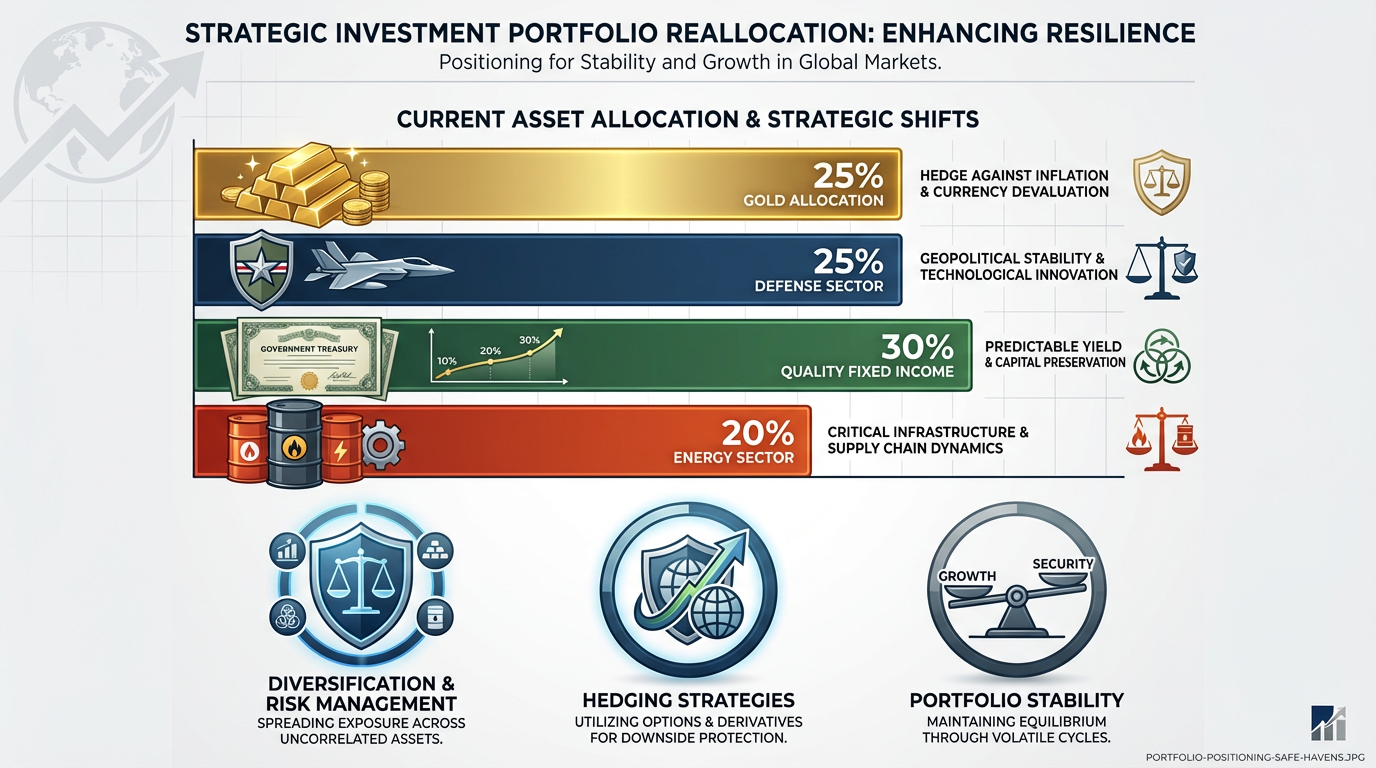

Energy: Higher oil prices are a direct tailwind for energy producers, particularly those with low production costs and strong balance sheets. But be selective—not all energy companies are created equal, and those with heavy exposure to conflict zones face operational risks.

Gold: The yellow metal has reasserted its role as the ultimate geopolitical hedge. A 4% gain in three weeks might seem modest, but in a world of negative real rates and currency debasement, gold’s role as a portfolio stabilizer has never been more relevant. At Savanti Investments, we’ve long advocated for a strategic allocation to gold as a non-correlated asset, and this environment validates that thesis.

The Losers

Airlines and Travel: Soaring jet fuel prices plus operational chaos from airspace closures is a toxic combination. The sector is losing $600 million per day, and there’s no end in sight. Avoid.

Consumer Cyclicals: Higher energy prices erode discretionary spending. Consumers feeling the pinch at the pump don’t splurge on new cars or luxury goods. Expect margin compression and earnings downgrades.

Emerging Markets (Selective): Energy-importing EMs with weak fiscal buffers are particularly vulnerable. Rising oil prices plus higher sovereign risk premia is a recipe for currency crises and capital flight. However, some EMs—particularly those benefiting from supply chain diversification like Mexico, Vietnam, and India—may actually emerge stronger.

The Strategic Playbook

At Savanti Investments, our approach to navigating this environment is grounded in three principles:

1. Maintain a Long-Term Focus: Don’t make rash decisions based on headlines. The long-term impact will depend on whether this conflict evolves into a sustained economic shock. Our quantitative models at QuantAI™ are designed to filter out noise and focus on structural trends, not short-term volatility.

2. Emphasize Quality and Diversification: In uncertain times, quality matters more than ever. Companies with strong balance sheets, consistent earnings, and sustainable competitive advantages will weather the storm. Diversification across asset classes and geographies remains the best defense against concentrated risk.

3. Implement Strategic Hedges: A modest allocation to gold, quality fixed income, and alternative strategies can reduce overall portfolio volatility. Our SavantTrade™ platform is actively monitoring volatility patterns and identifying tactical hedging opportunities in real-time.

The Contrarian View: Opportunity in Crisis

Here’s the uncomfortable truth: crises create opportunities. Not because we’re callous to the human suffering—the humanitarian toll of this conflict is immense and tragic. But because markets, in their fear, often misprice assets and create dislocations that disciplined investors can exploit.

History is littered with examples of investors who bought during geopolitical crises and were handsomely rewarded. The Gulf War. 9/11. The 2011 Arab Spring. In each case, the initial panic created buying opportunities for those with the courage and capital to act.

The key is distinguishing between temporary dislocations and permanent impairments. A high-quality company whose stock has been indiscriminately sold off due to broad market fear may represent exceptional value. A company with direct exposure to conflict zones or structural headwinds is a value trap.

This is where active management and quantitative analysis converge. At Savanti, we’re using our proprietary models to identify companies that have been oversold relative to their fundamentals, while simultaneously stress-testing portfolios for tail risk scenarios. It’s not about being a hero. It’s about being disciplined and data-driven.

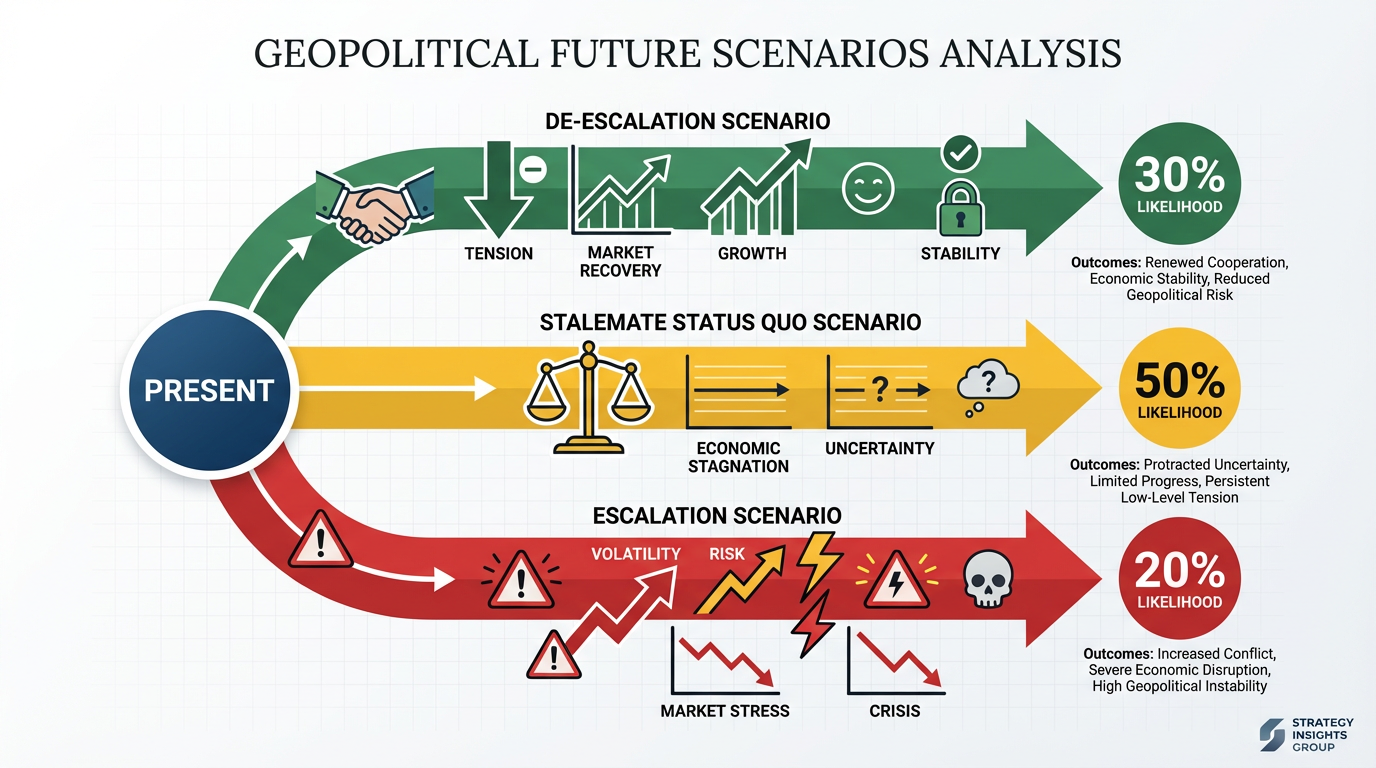

Looking Ahead: Three Scenarios

The future trajectory of this conflict—and its market impact—will depend on the strategic choices made by the primary combatants. I see three broad scenarios:

Scenario 1: Contained Conflict (Most Likely): The initial wave of strikes achieves its objectives, Iran’s response remains largely symbolic or limited to proxy actions, and the conflict doesn’t escalate into a wider regional war. In this scenario, oil prices recede from their peaks, equity markets recover, and we return to something resembling normalcy within 3-6 months. Market impact: sharp but short-lived.

Scenario 2: Prolonged Stalemate (Moderate Probability): Neither side achieves a decisive victory, leading to a grinding conflict characterized by periodic flare-ups, ongoing attacks on energy infrastructure, and persistent supply chain disruptions. Oil prices remain elevated but volatile, inflation stays sticky, and central banks remain paralyzed. This is the stagflation scenario, and it’s the most challenging for investors. Market impact: sustained volatility, sector rotation, compressed valuations.

Scenario 3: Full Escalation (Low Probability, High Impact): The conflict widens to include other regional powers, the Strait of Hormuz is effectively closed, and we face a full-blown energy crisis. This is the black swan scenario that triggers a global recession. Market impact: severe and prolonged, with double-digit equity declines and a flight to cash and gold.

My base case is Scenario 1, with a 60% probability. Scenario 2 gets 30%, and Scenario 3 gets 10%. But those probabilities are fluid and will shift based on developments on the ground.

The Bottom Line: Risk Is Real, But So Is Resilience

The geopolitical risk premium is back, and it’s not going away anytime soon. The US-Iran conflict has introduced a level of uncertainty into global markets that we haven’t seen in years, and the potential for further escalation is real.

But here’s what I’ve learned over decades in finance: markets are remarkably resilient. They’ve weathered world wars, financial crises, pandemics, and countless geopolitical shocks. They don’t move in straight lines, and they don’t reward panic.

What they do reward is discipline, diversification, and a willingness to look beyond the headlines to the underlying fundamentals. Yes, oil prices are elevated. Yes, volatility is high. Yes, there are real risks to the global economy. But there are also opportunities for those who can keep their heads while others are losing theirs.

At Savanti Investments, we’re not betting on any single scenario. We’re building portfolios that can withstand a range of outcomes, from rapid de-escalation to prolonged conflict. We’re using our quantitative tools to identify mispriced assets and our risk management frameworks to protect against tail risks. And we’re staying focused on the long-term structural trends—energy transition, supply chain resilience, technological innovation—that will define the next decade, regardless of what happens in the Middle East.

The geopolitical risk premium is real. But so is the resilience premium. And in the end, resilience always wins.

The question is: is your portfolio built for resilience?

Important Disclosures:

This article is provided for educational and informational purposes only and does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation for any security or investment strategy. The information contained herein is not intended to provide, and should not be relied upon for, investment advice.

Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. The views and opinions expressed are those of Braxton Tulin and Savanti Investments and are subject to change based on market and other conditions. There can be no assurance that any investment strategy will achieve its objectives or avoid losses.

Savanti Investments, QuantAI™, and SavantTrade™ are proprietary platforms and methodologies. References to these platforms are for illustrative purposes only and do not constitute an endorsement or recommendation.

This material is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local law or regulation. Investors should consult with their financial, legal, and tax advisors before making any investment decisions.

Securities offered through registered broker-dealers in accordance with Regulation D, Rule 506(c) of the Securities Act of 1933, as amended. Investments are limited to accredited investors only.