Disclaimer: This article is for educational and informational purposes only and is not investment advice. The content does not constitute a recommendation to buy or sell any security or financial instrument. Please consult with a qualified financial advisor before making any investment decisions.

When Governments Go On-Chain

On February 12, 2026, something remarkable happened that most people missed. The United Kingdom—a nation whose financial markets have been the backbone of global commerce for centuries—announced it would pilot the issuance of government bonds on a blockchain.

Let that sink in for a moment. We’re not talking about a startup experimenting with tokenization or a crypto-native company launching a new DeFi protocol. We’re talking about His Majesty’s Treasury putting sovereign debt on a distributed ledger.

The UK selected HSBC’s Orion platform to power its Digital Gilt Instrument (DIGIT) pilot, making Britain the first G7 nation to seriously test blockchain-based sovereign debt issuance. This isn’t just a technological curiosity—it’s a signal that the architecture of global capital markets is fundamentally changing.

What’s Happening: The Tokenization Wave Hits Government Bonds

The tokenization of government bonds represents the convergence of two powerful forces: the stability and trust of sovereign debt with the efficiency and programmability of blockchain technology.

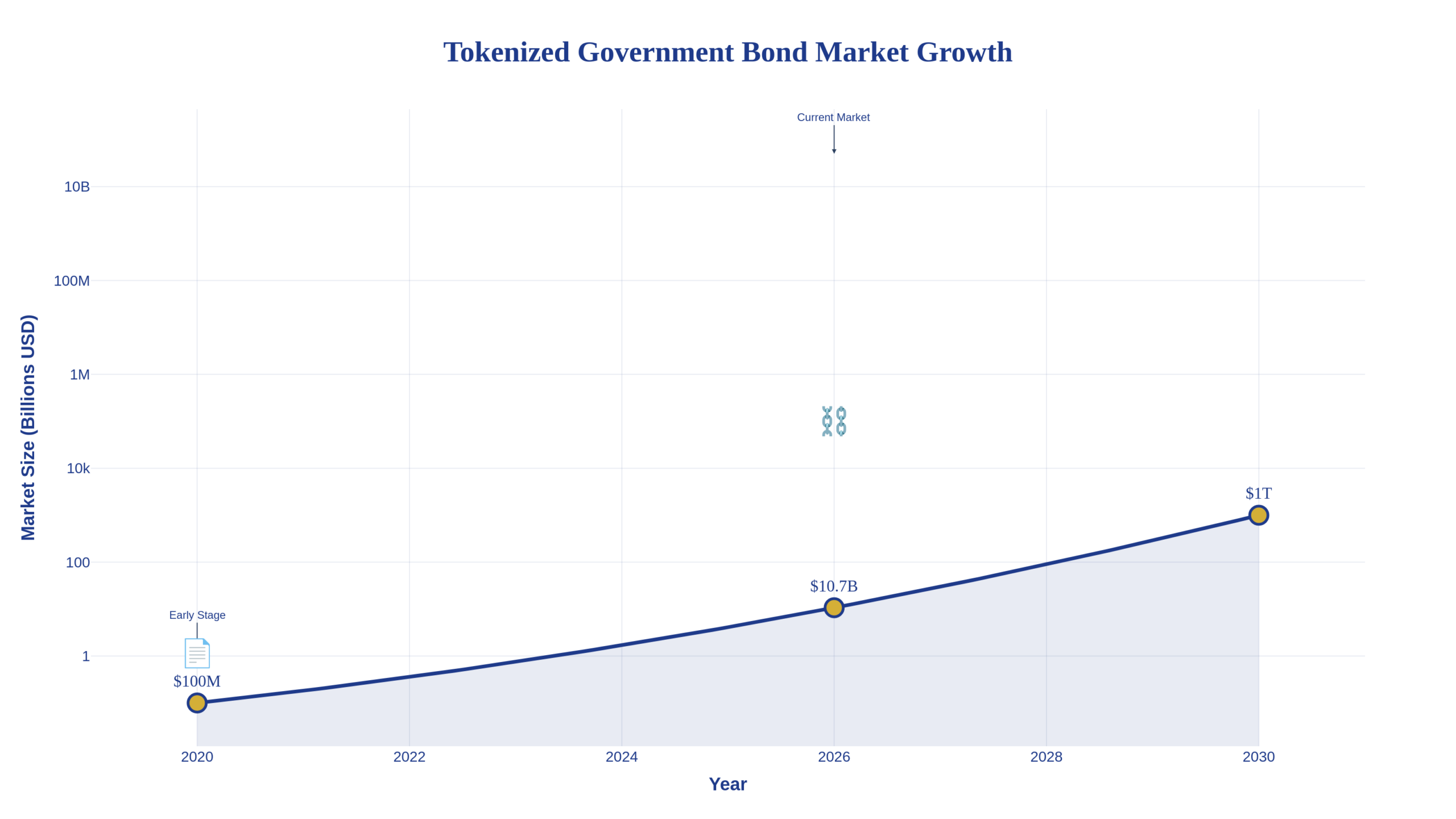

The numbers tell a compelling story. The market for tokenized U.S. Treasuries has exploded from under $100 million two years ago to over $10.7 billion today. That’s a 256% year-over-year growth rate. Industry projections suggest the broader tokenized bond market could reach $1 trillion by 2030.

Major financial institutions are leading the charge. BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) has amassed over $2.1 billion in assets. Franklin Templeton, Circle, and Ondo Finance have all launched tokenized treasury products that are seeing significant adoption. These aren’t speculative experiments—they’re institutional-grade products serving real demand for on-chain, yield-bearing assets.

But the UK’s DIGIT pilot takes this to another level entirely. When a G7 government decides to issue its own sovereign debt on a blockchain, it validates the entire thesis of tokenization. It says: “This technology is ready for the most critical, most regulated, most scrutinized financial instruments in the world.”

Why It Matters: The End of T+2 Settlement

To understand why this matters, you need to understand what’s broken in traditional bond markets.

When you buy a government bond today, the transaction doesn’t actually settle for one or two business days (T+1 or T+2). Your money is in limbo. The bond is in limbo. Counterparty risk exists. Capital is tied up. Intermediaries take their cut. The entire process is opaque, manual, and expensive.

Tokenization changes everything.

With blockchain-based bonds, settlement happens in seconds, not days. Smart contracts automate coupon payments, maturity redemptions, and compliance checks. Ownership is recorded on an immutable ledger that all parties can see in real-time. The concept of “delivery versus payment” becomes atomic—the bond and the payment exchange simultaneously in a single transaction, eliminating counterparty risk entirely.

For issuers like governments, this means cost reductions of 35-50% in issuance and servicing. For investors, it means 24/7 global markets, fractional ownership, and dramatically improved liquidity. For the financial system as a whole, it means less risk, more transparency, and greater capital efficiency.

At Savanti Investments, we’ve been tracking this trend closely. Our quantitative models—powered by our proprietary QuantAI™ platform—have been analyzing the implications of tokenized securities for portfolio construction and risk management. The efficiency gains are real, and they’re measurable.

The Technology: Smart Contracts Meet Sovereign Debt

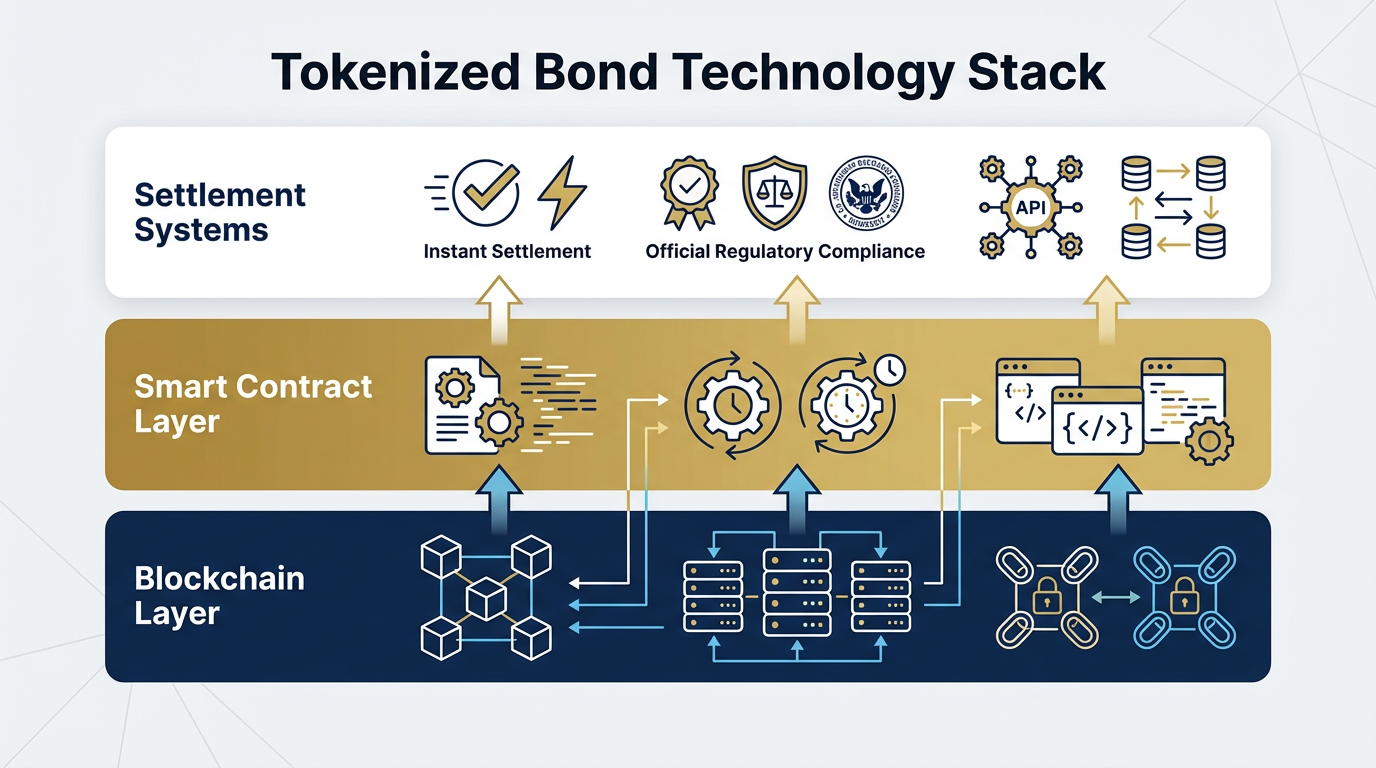

The infrastructure powering tokenized government bonds is elegant in its simplicity but profound in its implications.

At the foundation is blockchain—a distributed ledger that provides a single, verifiable source of truth for ownership and transaction history. Every transfer is recorded, timestamped, and immutable. No more reconciling multiple databases across different intermediaries.

On top of this sits the smart contract layer. These are self-executing programs that encode the bond’s entire lifecycle. When a coupon payment is due, the smart contract automatically distributes funds to current holders. When the bond matures, it automatically handles redemption. Compliance rules—KYC, AML, transfer restrictions—are embedded directly in the token’s code and enforced automatically.

The UK’s DIGIT pilot will run on HSBC’s Orion platform, which is built on the Canton Network—a privacy-focused blockchain designed for institutional finance. Orion has already facilitated over $3.5 billion in tokenized bond issuances, so this isn’t unproven technology. It’s battle-tested infrastructure being applied to the most important use case yet.

What excites me most is the potential for interoperability. As more governments and institutions adopt tokenization, we’ll need standards that allow these assets to move seamlessly across different blockchains and platforms. The development of common token standards and cross-chain protocols will be critical to unlocking the full potential of this market.

The Regulatory Reality: Substance Over Form

One of the most common misconceptions about tokenized securities is that they exist in some regulatory gray area. They don’t.

Regulators globally have been remarkably consistent in their approach: if it looks like a security, acts like a security, and quacks like a security, it’s a security—regardless of whether it’s on a blockchain or not. This “substance over form” principle means tokenized government bonds are subject to the same securities laws as traditional bonds.

In the U.S., the SEC applies the Howey Test. Tokenized bonds clearly qualify as securities and must be registered or issued under an exemption like Regulation D or Regulation A+. In the EU, they fall under MiFID II, though the DLT Pilot Regime provides a regulatory sandbox for testing. The UK’s Digital Securities Sandbox, which will host the DIGIT pilot, offers a similar controlled environment with modified regulations.

Singapore, Hong Kong, Switzerland, and Japan have all established clear frameworks for tokenized securities. The regulatory landscape is fragmented, yes, but it’s not uncertain. The rules exist—they’re just different in each jurisdiction.

The challenge for issuers is navigating this patchwork, especially for cross-border offerings. But the opportunity is enormous. Jurisdictions that create clear, supportive frameworks will attract capital and innovation. Those that don’t will be left behind.

Real-World Implications: From TradFi to DeFi

The most fascinating aspect of tokenized government bonds isn’t what they do for traditional finance—it’s how they bridge the gap between TradFi and DeFi.

In the crypto ecosystem, there’s been a persistent challenge: how do you create stable, low-risk yield without relying on centralized stablecoins or risky DeFi protocols? Tokenized Treasuries solve this problem elegantly. They bring real-world, government-backed yield on-chain.

We’re already seeing tokenized Treasuries used as collateral in DeFi lending protocols, as backing for stablecoins, and as the underlying asset for structured products. As the market matures, I expect these tokens to become the premier form of high-quality collateral across the entire DeFi ecosystem.

This has profound implications for capital efficiency. Imagine a world where your government bond holdings can be used as collateral for a loan, which you then deploy in a quantitative trading strategy, all while continuing to earn the bond’s yield. That’s the power of composability—and it’s only possible when these assets are tokenized and programmable.

At Savanti, we’re exploring how tokenized securities can be integrated into our SavantTrade™ platform, which provides institutional-grade execution for digital assets. The ability to trade government bonds 24/7 with instant settlement opens up entirely new strategies for portfolio management and risk hedging.

The Risks: What Could Go Wrong

I’d be remiss if I didn’t address the risks, because they’re real and significant.

Smart contract vulnerabilities are the most obvious concern. A bug in the code governing a multi-billion-dollar bond issuance could be catastrophic. Rigorous audits are essential, but they’re not foolproof. The history of DeFi is littered with hacks and exploits.

Custody is another challenge. With tokenized assets, ownership is controlled by private keys. Lose the key, lose the asset—permanently. For institutions managing billions in assets, this requires enterprise-grade custody solutions with robust security and recovery mechanisms.

Regulatory fragmentation remains a headwind. The lack of harmonized global standards creates complexity and compliance costs. Legal enforceability of smart contracts is still being established in many jurisdictions.

And then there’s the liquidity question. While tokenization promises enhanced liquidity, the reality in these early stages is that secondary markets can be thin. Liquidity may be fragmented across different platforms and blockchains, making it difficult to execute large trades without market impact.

These aren’t insurmountable challenges, but they require careful risk management and a realistic assessment of where the technology is today versus where it needs to be.

The Future: A $1 Trillion Market

So where does this go from here?

The success of the UK’s DIGIT pilot will be a critical inflection point. If His Majesty’s Treasury can demonstrate that blockchain-based sovereign debt issuance is more efficient, more secure, and more cost-effective than traditional methods, other G7 nations will follow. The blueprint will exist.

I expect we’ll see a gradual but accelerating adoption curve. More governments will launch pilots. More institutional investors will allocate to tokenized products. More DeFi protocols will integrate these assets as collateral. The infrastructure will mature, standards will emerge, and liquidity will deepen.

The $1 trillion projection for tokenized bonds by 2030 is ambitious but achievable. That would represent roughly 100x growth from today’s ~$10 billion market. It sounds aggressive, but remember: this market was essentially zero just two years ago.

At Convirtio, our marketing automation platform, we’re seeing similar exponential adoption curves in AI-powered tools. When a technology reaches a certain threshold of utility and ease of use, adoption doesn’t happen linearly—it happens exponentially.

The long-term vision is a financial system built on programmable, transparent, and accessible digital infrastructure. Government bonds—the bedrock of global finance—will be issued, traded, and settled on blockchains. Investors around the world will have 24/7 access to these markets. Capital will flow more efficiently. Risk will be managed more effectively.

This isn’t science fiction. It’s happening right now, one pilot program at a time.

The Bottom Line

The tokenization of government bonds is more than a technological upgrade—it’s a fundamental reimagining of how capital markets work.

When the UK issues its first digital gilt, it won’t just be a milestone for blockchain technology. It will be a signal that the future of finance is programmable, transparent, and accessible in ways that were impossible with legacy infrastructure.

For investors, this creates new opportunities for yield, liquidity, and portfolio diversification. For governments, it offers a path to more efficient debt management and lower borrowing costs. For the financial system as a whole, it promises greater stability, transparency, and resilience.

The transition won’t happen overnight, and the path forward will have obstacles. But the direction is clear. The architecture of global capital markets is being rebuilt on a blockchain foundation, and government bonds are leading the way.

The question isn’t whether this will happen. The question is how quickly—and who will be positioned to benefit when it does.

Important Disclosures:

This article is provided for educational and informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice. The information presented should not be construed as a recommendation to purchase or sell any security or financial instrument. Savanti Investments and its affiliates do not guarantee the accuracy or completeness of the information provided.

Investing in tokenized securities, digital assets, and blockchain-based instruments involves substantial risk, including the possible loss of principal. These markets are highly volatile and may be subject to regulatory changes, technological failures, cybersecurity risks, and liquidity constraints. Past performance is not indicative of future results.

This content may discuss securities offered pursuant to Regulation D, Rule 506(c) of the Securities Act of 1933, which are available only to accredited investors as defined in Rule 501 of Regulation D. Prospective investors should carefully review all offering materials and consult with their own legal, tax, and financial advisors before making any investment decision.

Savanti Investments, QuantAI™, SavantTrade™, and Convirtio are trademarks of their respective entities. References to these platforms are for illustrative purposes and do not constitute an offer to sell or a solicitation of an offer to buy any securities.

© 2026 Braxton Tulin. All rights reserved.